Insights

How EU ESG Regulations Impact Startup Value Creation and Risk Management

26 November 2025

Insights

How EU ESG Regulations Impact Startup Value Creation and Risk Management

26 November 2025

D espite the simplification and downscaling of sustainability in the context of the 2025 Omnibus discussions, a recent UN Global Compact-Accenture CEO study1 reveals a compelling shift: 88% of CEOs now recognize a stronger business case for sustainability. The message is clear — sustainability is no longer a peripheral issue but a central driver of resilience, innovation, and long-term value creation (Morgan Stanley, 2025;2 World Economic Forum, 2025;3 Deloitte, 20254).

This growing recognition is already translating into tangible expectations across the business landscape. Banks, investors, and large corporations which rely on non-listed SMEs and startups as suppliers are intensifying their demand for sustainability-related data. Startups are increasingly expected to report on ESG issues, a trend largely propelled by evolving regulatory frameworks (EFRAG, 2024;5 KPMG, 2025a;6 EBA, 20257).

For instance, under the EU Capital Requirements Directive VI [Directive (EU) 2024/1619]8 and its Danish implementation, L193B (Act no. 712 of 20/06/2025)9, financial institutions are required to integrate ESG factors into their strategic planning, risk management, and lending practices. As a result, banks must incorporate sustainability risks into their credit assessments. Moreover, the newly adopted Ecodesign Regulation for Sustainable Products (ESPR) [Regulation (EU) 2024/1781]10 aims to significantly enhance the sustainability of products placed on the EU market. This regulation mandates that manufacturers comply with stringent sustainability criteria.

As sustainability regulations become the norm, perceptions of ESG have shifted from a financial burden to a value enabler. For startups, integrating ESG early into their business strategy has increasingly become essential. Doing so accelerates access to external financing, enhances market accessibility, and meets stakeholders’ expectations.

To further illustrate how ESG serves as a value enabler under the EU regulations, we will explore how it is anchored in two core business objectives: value creation and risk management.

D espite the simplification and downscaling of sustainability in the context of the 2025 Omnibus discussions, a recent UN Global Compact-Accenture CEO study1 reveals a compelling shift: 88% of CEOs now recognize a stronger business case for sustainability. The message is clear — sustainability is no longer a peripheral issue but a central driver of resilience, innovation, and long-term value creation (Morgan Stanley, 2025;2 World Economic Forum, 2025;3 Deloitte, 20254).

This growing recognition is already translating into tangible expectations across the business landscape. Banks, investors, and large corporations which rely on non-listed SMEs and startups as suppliers are intensifying their demand for sustainability-related data. Startups are increasingly expected to report on ESG issues, a trend largely propelled by evolving regulatory frameworks (EFRAG, 2024;5 KPMG, 2025a;6 EBA, 20257).

For instance, under the EU Capital Requirements Directive VI [Directive (EU) 2024/1619]8 and its Danish implementation, L193B (Act no. 712 of 20/06/2025)9, financial institutions are required to integrate ESG factors into their strategic planning, risk management, and lending practices. As a result, banks must incorporate sustainability risks into their credit assessments. Moreover, the newly adopted Ecodesign Regulation for Sustainable Products (ESPR) [Regulation (EU) 2024/1781]10 aims to significantly enhance the sustainability of products placed on the EU market. This regulation mandates that manufacturers comply with stringent sustainability criteria.

As sustainability regulations become the norm, perceptions of ESG have shifted from a financial burden to a value enabler. For startups, integrating ESG early into their business strategy has increasingly become essential. Doing so accelerates access to external financing, enhances market accessibility, and meets stakeholders’ expectations.

To further illustrate how ESG serves as a value enabler under the EU regulations, we will explore how it is anchored in two core business objectives: value creation and risk management.

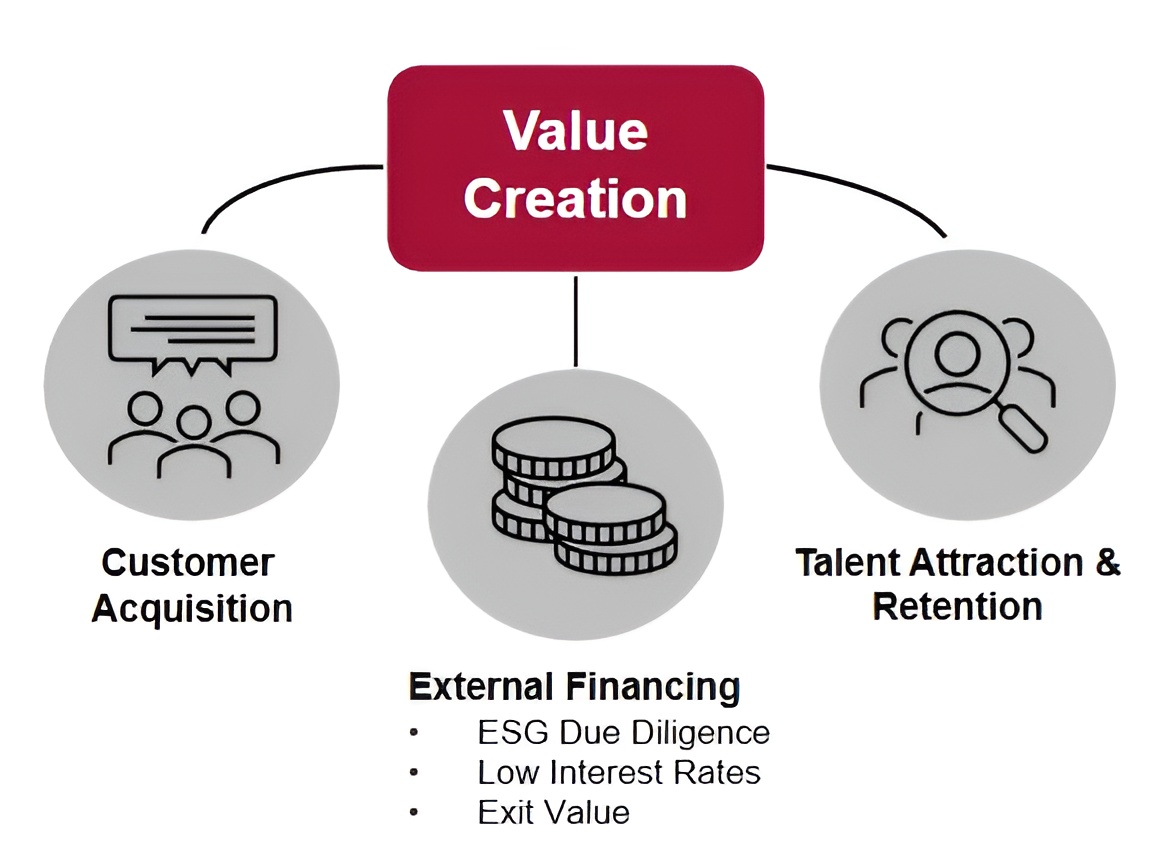

Value Creation

Value creation in startups is often driven by three core dimensions:

- securing external financing,

- acquiring customers, and

- attracting and retaining talent

— all increasingly influenced by ESG regulations (Exhibit 1).

Value Creation

Value creation in startups is often driven by three core dimensions:

- securing external financing,

- acquiring customers, and

- attracting and retaining talent

— all increasingly influenced by ESG regulations (Exhibit 1).

Exhibit 1

Three core dimensions for startups’ value creation: external financing, customer acquisition, and talent attraction and retention.

© ESGEra Consulting

External Financing

Securing funding to enable growth is always on top of the agenda for startups. Today, the emphasis on ESG has become prevalent in the financial landscape, particularly among investors and banks.

The focus on ESG has intensified in recent years due to mounting legal pressure, with investment institutions increasingly assessing the underlying sustainability risks of businesses. This may involve evaluating climate-related risks, energy consumption, workplace conditions, social impact and diversity, and responsible practices across the value chain (Novo Holdings, 2024a;11 Novo Holdings, 2024b;12 EIFO, n.d.13). Furthermore, investors are increasingly treating ESG as a key factor for an exit, particularly in relation to Initial Public Offering (IPO) and merger and acquisition (M&A) scenarios. In the pre-IPO phase, ESG performance is seen as a potential risk factor that can influence both valuation and timing. EY reports that venture capitalists and private equity investors actively assess sustainability risks early, as these may reduce company value at exit (EY, 2022).14 A global survey by BCG and Gibson Dunn (BCG, 2024)15 also reveals that ESG due diligence has become indispensable in M&A and dealmakers now view ESG as essential for both risk mitigation and value preservation and enhancement.

Banks, specifically, have adopted structured and methodical approaches to ESG, often assigning individual ESG scores to classify their clients (KPMG, 2023;16 MSCI, 202417). Through sustainability-linked financing, banks such as Danske Bank and Jyske Bank offer interest rates that are directly tied to a company’s ability to meet predefined sustainability targets. If these targets are met, the company benefits from lower interest rates; if not, the rates increase (Danske Bank, n.d.;18 Jyske Bank, n.d.19). For instance, COWI pays less for its credit facilities when it successfully reduces greenhouse gas emissions from business travel and achieves its gender diversity goals at senior leadership levels. Conversely, failure to meet these targets results in a higher premium (COWI, n.d.).20

Customer Acquisition

The evolving landscape of sustainability regulations increasingly compels customers — especially public authorities — to prioritize ESG performance when selecting suppliers. For instance, the Green Public Procurement Rule requires public buyers to prioritize products of concern that meet the highest standards of sustainability and circularity ([Regulation (EU) 2024/1781;10 European Commission, n.d.21).

Furthermore, large companies that are required to disclose ESG data across their supply chains are increasingly demanding corresponding information from their suppliers to meet regulatory reporting obligations. This regulatory pressure is cascading through the value chain, compelling smaller firms and startups to monitor and report their own ESG performance to remain eligible as business partners. As ESG regulations continue to evolve, compliance is becoming a prerequisite for participation in many supply networks (Thomson Reuters, 2024).22

Talent Attraction and Retention

ESG regulations now also affect talent attraction and retention due to the increasing transparency of a company’s social, environmental, and governance practices. Firms are, and will increasingly be, required — under legal frameworks such as the Corporate Sustainability Reporting Directive (CSRD) — to disclose information on gender diversity, pay gap, work-life balance and health and safety [Regulation (EU) 2023/2772].23 When choosing an employer, these disclosures provide talent prospects with credible insights into the company’s values, workplace culture, and long-term commitment to responsible business conduct.

Companies with weak social practices have been shown to face up to higher attrition rates compared to those with strong engagement strategies (Work Institute, 2025).24 According to PwC’s 2024 Global Workforce ESG Study (PwC, 2024),25 68.6% of employees choose their employer based on ESG policies and practices, while 65.5% decide to stay for the same reasons. Mark Gibson, Global Head of Technology, Media & Telecommunications KPMG, further emphasizes that “in tech, employees have high expectations for each of the three areas of ESG” (KPMG, 2025b).26 At the same time, a report from McKinsey & Company (2025)27 projects that, in the EU alone, the tech talent gap could be 1.4 million to 3.9 million people by 2027.

Thus, with ESG disclosure obligations, strong ESG practices are no longer just “nice-to-have”; they are now a critical tool to attract and retain top talent, differentiate from competitors, and mitigate the tech talent shortage risks.

Exhibit 1

Three core dimensions for startups’ value creation: external financing, customer acquisition, and talent attraction and retention.

© ESGEra Consulting

External Financing

Securing funding to enable growth is always on top of the agenda for startups. Today, the emphasis on ESG has become prevalent in the financial landscape, particularly among investors and banks.

The focus on ESG has intensified in recent years due to mounting legal pressure, with investment institutions increasingly assessing the underlying sustainability risks of businesses. This may involve evaluating climate-related risks, energy consumption, workplace conditions, social impact and diversity, and responsible practices across the value chain (Novo Holdings, 2024a;11 Novo Holdings, 2024b;12 EIFO, n.d.13). Furthermore, investors are increasingly treating ESG as a key factor for an exit, particularly in relation to Initial Public Offering (IPO) and merger and acquisition (M&A) scenarios. In the pre-IPO phase, ESG performance is seen as a potential risk factor that can influence both valuation and timing. EY reports that venture capitalists and private equity investors actively assess sustainability risks early, as these may reduce company value at exit (EY, 2022).14 A global survey by BCG and Gibson Dunn (BCG, 2024)15 also reveals that ESG due diligence has become indispensable in M&A and dealmakers now view ESG as essential for both risk mitigation and value preservation and enhancement.

Banks, specifically, have adopted structured and methodical approaches to ESG, often assigning individual ESG scores to classify their clients (KPMG, 2023;16 MSCI, 202417). Through sustainability-linked financing, banks such as Danske Bank and Jyske Bank offer interest rates that are directly tied to a company’s ability to meet predefined sustainability targets. If these targets are met, the company benefits from lower interest rates; if not, the rates increase (Danske Bank, n.d.;18 Jyske Bank, n.d.19). For instance, COWI pays less for its credit facilities when it successfully reduces greenhouse gas emissions from business travel and achieves its gender diversity goals at senior leadership levels. Conversely, failure to meet these targets results in a higher premium (COWI, n.d.).20

Customer Acquisition

The evolving landscape of sustainability regulations increasingly compels customers — especially public authorities — to prioritize ESG performance when selecting suppliers. For instance, the Green Public Procurement Rule requires public buyers to prioritize products of concern that meet the highest standards of sustainability and circularity ([Regulation (EU) 2024/1781;10 European Commission, n.d.21).

Furthermore, large companies that are required to disclose ESG data across their supply chains are increasingly demanding corresponding information from their suppliers to meet regulatory reporting obligations. This regulatory pressure is cascading through the value chain, compelling smaller firms and startups to monitor and report their own ESG performance to remain eligible as business partners. As ESG regulations continue to evolve, compliance is becoming a prerequisite for participation in many supply networks (Thomson Reuters, 2024).22

Talent Attraction and Retention

ESG regulations now also affect talent attraction and retention due to the increasing transparency of a company’s social, environmental, and governance practices. Firms are, and will increasingly be, required — under legal frameworks such as the Corporate Sustainability Reporting Directive (CSRD) — to disclose information on gender diversity, pay gap, work-life balance and health and safety [Regulation (EU) 2023/2772].23 When choosing an employer, these disclosures provide talent prospects with credible insights into the company’s values, workplace culture, and long-term commitment to responsible business conduct.

Companies with weak social practices have been shown to face up to higher attrition rates compared to those with strong engagement strategies (Work Institute, 2025).24 According to PwC’s 2024 Global Workforce ESG Study (PwC, 2024),25 68.6% of employees choose their employer based on ESG policies and practices, while 65.5% decide to stay for the same reasons. Mark Gibson, Global Head of Technology, Media & Telecommunications KPMG, further emphasizes that “in tech, employees have high expectations for each of the three areas of ESG” (KPMG, 2025b).26 At the same time, a report from McKinsey & Company (2025)27 projects that, in the EU alone, the tech talent gap could be 1.4 million to 3.9 million people by 2027.

Thus, with ESG disclosure obligations, strong ESG practices are no longer just “nice-to-have”; they are now a critical tool to attract and retain top talent, differentiate from competitors, and mitigate the tech talent shortage risks.

Risk Management

The regulatory landscape within the EU is evolving rapidly, bringing with it increasingly complex compliance requirements…

Risk Management

The regulatory landscape within the EU is evolving rapidly, bringing with it increasingly complex compliance requirements…

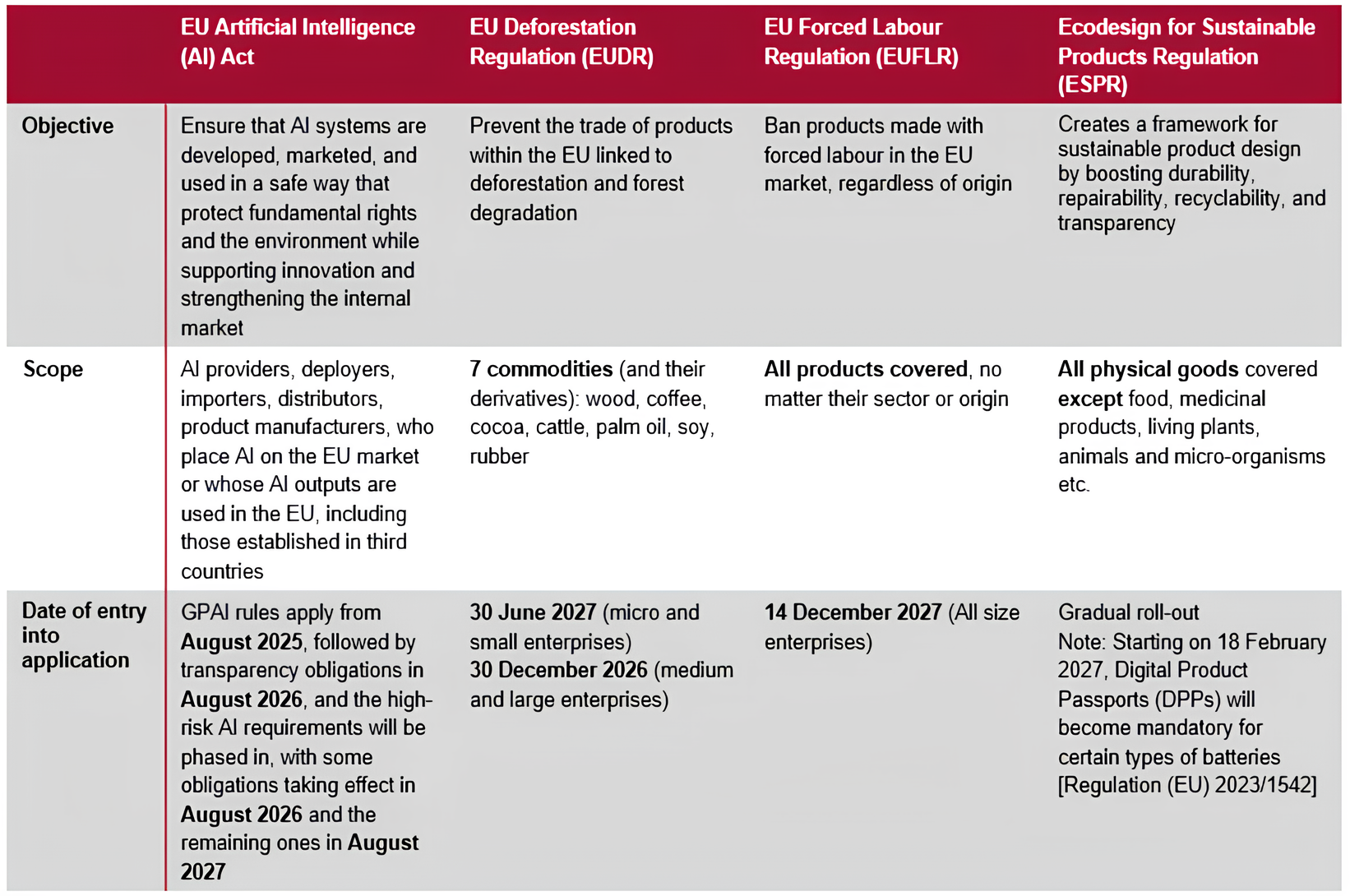

The regulatory landscape within the EU is evolving rapidly, bringing with it increasingly complex compliance requirements. While the most prominent sustainability directive, the CSRD, does not apply to non-listed SMEs and is currently undergoing delays and significant simplifications, other regulations — such as the EU Artificial Intelligence (AI) Act, the Regulation on Deforestation-free Products (EUDR), the EU Forced Labour Regulation and the ESPR (Table 1) — still pertain to SMEs and microenterprises. The EU AI Act promotes trustworthy, human-centred AI in the EU, protecting health, fundamental rights, democracy, and the environment. The EUDR targets specific commodities to ensure they are deforestation-free and legally produced, while the ESPR applies to almost all physical products placed on the EU market, promoting sustainability, durability, and circularity throughout their life cycle. Meanwhile, the Forced Labour Regulation seeks to prevent products made with forced labour from being placed on, sold in or exported from the EU market.

Table 1

The four EU ESG regulations that are highly relevant for microenterprises and SMEs — the EU AI Act, the EU Deforestation Regulation, the EU Forced Labour Regulation, and the Ecodesign for Sustainable Products Regulation

© ESGEra Consulting

With this in mind, proactive engagement with regulatory developments supports internal risk management and helps startups avoid costly retrofits or reputational setbacks as enforcement tightens (Deloitte, 2023;28 BCG, 202229). Furthermore, compliance readiness facilitates smoother entry into key EU markets, where regulatory alignment is a prerequisite for expansion (OECD, 2022).30

Conclusion

The EU’s evolving ESG regulatory framework is reshaping the way startups approach growth, governance, and risk. By proactively aligning value creation with regulatory expectations, startups can turn ESG compliance into a source of competitive advantage. Early adoption of structured ESG practices not only mitigates future risks but also enables startups to secure favorable financing access new customers, and attract and retain talents.

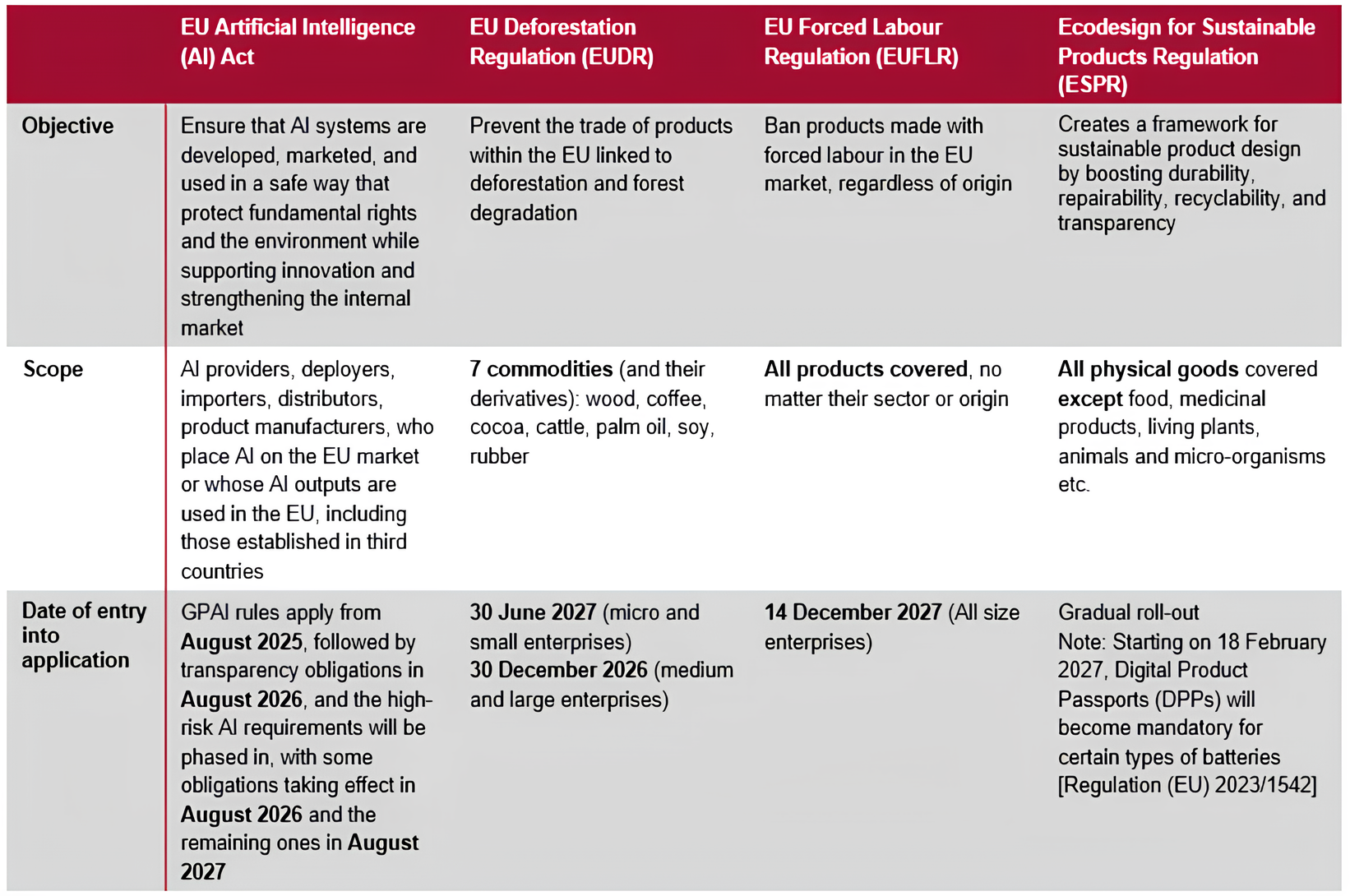

The regulatory landscape within the EU is evolving rapidly, bringing with it increasingly complex compliance requirements. While the most prominent sustainability directive, the CSRD, does not apply to non-listed SMEs and is currently undergoing delays and significant simplifications, other regulations — such as the EU Artificial Intelligence (AI) Act, the Regulation on Deforestation-free Products (EUDR), the EU Forced Labour Regulation and the ESPR (Table 1) — still pertain to SMEs and microenterprises. The EU AI Act promotes trustworthy, human-centred AI in the EU, protecting health, fundamental rights, democracy, and the environment. The EUDR targets specific commodities to ensure they are deforestation-free and legally produced, while the ESPR applies to almost all physical products placed on the EU market, promoting sustainability, durability, and circularity throughout their life cycle. Meanwhile, the Forced Labour Regulation seeks to prevent products made with forced labour from being placed on, sold in or exported from the EU market.

Table 1

The four EU ESG regulations that are highly relevant for microenterprises and SMEs — the EU AI Act, the EU Deforestation Regulation, the EU Forced Labour Regulation, and the Ecodesign for Sustainable Products Regulation

© ESGEra Consulting

With this in mind, proactive engagement with regulatory developments supports internal risk management and helps startups avoid costly retrofits or reputational setbacks as enforcement tightens (Deloitte, 2023;28 BCG, 202229). Furthermore, compliance readiness facilitates smoother entry into key EU markets, where regulatory alignment is a prerequisite for expansion (OECD, 2022).30

Conclusion

The EU’s evolving ESG regulatory framework is reshaping the way startups approach growth, governance, and risk. By proactively aligning value creation with regulatory expectations, startups can turn ESG compliance into a source of competitive advantage. Early adoption of structured ESG practices not only mitigates future risks but also enables startups to secure favorable financing access new customers, and attract and retain talents.

1.

UN Global Compact and Accenture (2025) Turning the Key. Unlocking the next Era of Sustainability Leadership. [online] Available here.

2.

Morgan Stanley (2025) Companies See Sustainability as a Way to Create Value. [online] Available here.

3.

World Economic Forum (2025) Unlocking green growth: Sustainability as a key driver of corporate innovation. [online] Available here.

4.

Deloitte (2025) 2025 C-suite Sustainability Report. [online] Available here.

5.

EFRAG (2024) Voluntary Reporting Standards for SMEs. [online] Available here.

6.

KPMG (2025a) ESG risks in 2025: Responding to regulatory and supervisory pressure. [online] Available here.

7.

European Banking Authority (EBA) (2025) Final Report. Guidelines on the management of environmental, social and governance (ESG) risks. [online] Available here.

8.

Directive (EU) 2024/1619 of the European Parliament and of the Council of 31 May 2024 amending Directive 2013/36/EU as regards supervisory powers, sanctions, third-country branches, and environmental, social and governance risks PE/79/2023/REV/1 (OJ L, 2024/1619, 19.6.2024, ELI: http://data.europa.eu/eli/dir/2024/1619/oj )

9.

Act no. 712 of 20/06/2025 (2025) Act amending the Financial Business Act, the Alternative Investment Fund Managers Act, etc., the Investment Associations Act, etc., the Money Laundering Act and various other acts (in Danish: LOV nr 712 af 20/06/2025 (2025) Lov om ændring af lov om finansiel virksomhed, lov om forvaltere af alternative investeringsfonde m.v., lov om investeringsforeninger m.v., hvidvaskloven og forskellige andre love) [online] Available here.

10.

Regulation (EU) 2024/1781 of the European Parliament and of the Council of 13 June 2024 establishing a framework for the setting of ecodesign requirements for sustainable products, amending Directive (EU) 2020/1828 and Regulation (EU) 2023/1542 and repealing Directive 2009/125/EC (OJ L, 2024/1781, 28.6.2024, ELI: http://data.europa.eu/eli/reg/2024/1781/oj)

11.

Novo Holdings (2024a) Responsible Investment Report. [online] Available here.

12.

Novo Holdings (2024b) Responsible Investment Policy. [online] Available here.

13.

Danmarks Eksport & Investeringsfond (EIFO) (n.d.) EIFO’s approach to ESG. [online] Available here.

14.

EY (2022) Why successful investors focus on sustainability pre- and post- IPO. [online] Available here.

15.

BCG (2024) The Payoffs and Pitfalls of ESG Due Diligence. [online] Available here.

16.

KPMG (2023) ESG Risk Survey for Banks. [online] Available here.

17.

MSCI (2024) ESG Ratings. Assess companies on their financially relevant sustainability risks and opportunities. [online] Available here.

18.

Danske Bank (n.d.) Sustainability-linked guarantees. [online] Available here.

19.

Jyske Bank (n.d.) ESG Financing and grants. [online] Available here.

20.

COWI (n.d.) Loan agreements linked to COWI’s ESG performance. [online] Available here.

21.

European Commission (n.d.) Green Public Procurement. [online] Available here.

22.

Thomsen Reuters (2024) New study reveals how ESG is a growing factor in global trade & supply chain resilience. [online] Available here.

23.

Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards OJ L, 2023/2772, 22.12.2023, ELI: http://data.europa.eu/eli/reg_del/2023/2772/oj

24.

Work Institute (2025) Retention Report. [online] Available here.

25.

PwC (2024) Global Workforce ESG Preferences Study 2024. [online] Available here.

26.

KPMG (2025b) KPMG global tech report: Technology insights. [online] Available here.

27.

McKinsey & Company (2025) Tech talent gap: Addressing an ongoing challenge. [online] Available here.

28.

Deloitte (2023) Managing the risk of ESG misconduct. [online] Available here.

29.

BCG (2022) ESG Compliance in an Era of Tighter Regulations. [online] Available here.

30.

OECD (2022) Promoting Start‑Ups and Scale‑Ups in Denmark’s Sector Strongholds and Emerging Industries. [online] Available here.

1. UN Global Compact and Accenture (2025) Turning the Key. Unlocking the next Era of Sustainability Leadership. [online] Available here.

2. Morgan Stanley (2025) Companies See Sustainability as a Way to Create Value. [online] Available here.

3. World Economic Forum (2025) Unlocking green growth: Sustainability as a key driver of corporate innovation. [online] Available here.

4. Deloitte (2025) 2025 C-suite Sustainability Report. [online] Available here.

5. EFRAG (2024) Voluntary Reporting Standards for SMEs. [online] Available here.

6. KPMG (2025a) ESG risks in 2025: Responding to regulatory and supervisory pressure. [online] Available here.

7. European Banking Authority (EBA) (2025) Final Report. Guidelines on the management of environmental, social and governance (ESG) risks. [online] Available here.

8. Directive (EU) 2024/1619 of the European Parliament and of the Council of 31 May 2024 amending Directive 2013/36/EU as regards supervisory powers, sanctions, third-country branches, and environmental, social and governance risks PE/79/2023/REV/1 (OJ L, 2024/1619, 19.6.2024, ELI: http://data.europa.eu/eli/dir/2024/1619/oj )

9. Act no. 712 of 20/06/2025 (2025) Act amending the Financial Business Act, the Alternative Investment Fund Managers Act, etc., the Investment Associations Act, etc., the Money Laundering Act and various other acts (in Danish: LOV nr 712 af 20/06/2025 (2025) Lov om ændring af lov om finansiel virksomhed, lov om forvaltere af alternative investeringsfonde m.v., lov om investeringsforeninger m.v., hvidvaskloven og forskellige andre love) [online] Available here.

10. Regulation (EU) 2024/1781 of the European Parliament and of the Council of 13 June 2024 establishing a framework for the setting of ecodesign requirements for sustainable products, amending Directive (EU) 2020/1828 and Regulation (EU) 2023/1542 and repealing Directive 2009/125/EC (OJ L, 2024/1781, 28.6.2024, ELI: http://data.europa.eu/eli/reg/2024/1781/oj)

11. Novo Holdings (2024a) Responsible Investment Report. [online] Available here.

12. Novo Holdings (2024b) Responsible Investment Policy. [online] Available here.

13. Danmarks Eksport & Investeringsfond (EIFO) (n.d.) EIFO’s approach to ESG. [online] Available here.

14. EY (2022) Why successful investors focus on sustainability pre- and post- IPO. [online] Available here.

15. BCG (2024) The Payoffs and Pitfalls of ESG Due Diligence. [online] Available here.

16. KPMG (2023) ESG Risk Survey for Banks. [online] Available here.

17. MSCI (2024) ESG Ratings. Assess companies on their financially relevant sustainability risks and opportunities. [online] Available here.

18. Danske Bank (n.d.) Sustainability-linked guarantees. [online] Available here.

19. Jyske Bank (n.d.) ESG Financing and grants. [online] Available here.

20. COWI (n.d.) Loan agreements linked to COWI’s ESG performance. [online] Available here.

21. European Commission (n.d.) Green Public Procurement. [online] Available here.

22. Thomsen Reuters (2024) New study reveals how ESG is a growing factor in global trade & supply chain resilience. [online] Available here.

23. Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards OJ L, 2023/2772, 22.12.2023, ELI: http://data.europa.eu/eli/reg_del/2023/2772/oj

24. Work Institute (2025) Retention Report. [online] Available here.

25. PwC (2024) Global Workforce ESG Preferences Study 2024. [online] Available here.

26. KPMG (2025b) KPMG global tech report: Technology insights. [online] Available here.

27. McKinsey & Company (2025) Tech talent gap: Addressing an ongoing challenge. [online] Available here.

28. Deloitte (2023) Managing the risk of ESG misconduct. [online] Available here.

29. BCG (2022) ESG Compliance in an Era of Tighter Regulations. [online] Available here.

30. OECD (2022) Promoting Start‑Ups and Scale‑Ups in Denmark’s Sector Strongholds and Emerging Industries. [online] Available here.

ABOUT THE AUTHOR(S)

This article was written by Pauline Reese, a Sustainability Consultant at ESGEra Consulting in Copenhagen.

To request a follow-up with an expert at ESGEra Consulting, please reach out to contact@esgeraconsulting.com.

Our Next Insight:

Startup-fit Double Materiality Assessment

With the growing ESG regulatory landscape, startups face increasing pressure of compliance while creating value and mitigating risks.

To achieve both, a value-driven and compliant ESG strategy is essential. However, developing such a robust and credible strategy requires a clear understanding of which ESG issues truly matter, both to the business and its stakeholders. This is where the Double Materiality Assessment (DMA) becomes crucial. It provides an analytical foundation to identify key impacts, risks, and opportunities (IROs), ensuring that ESG priorities are both compliant and strategically relevant.

Show More

Nevertheless, the DMA framework, as stipulated by the CSRD, is inherently resource-intensive, demanding extensive data collection, cross-functional stakeholder engagement, and financial investment — resources that are often beyond the reach of startups. In addition, it may not capture the full IROs for startups from other ESG regulations.

To overcome these challenges, a “Startup-Fit DMA” is needed — a lighter, more targeted version that maintains analytical rigor while tailoring scope and effort to the realities of resource-constrained startups. This approach enables startups to focus on the most material ESG topics aligned with both EU regulations and long-term value creation.